Opening Brief

At a Glance

Our Client

Our client, a global supplier active across electronics manufacturing, industrial technology, and automotive electronics, was confronted with significant price increase demands from its PCBA suppliers. The increases were justified by rising raw material costs, but without structured cost transparency, the procurement team had no reliable basis to validate or challenge these claims.

The scope covered 45 PCBA variants sourced from 3 suppliers, with a total procurement volume exceeding EUR 50 million. Each variant came with its own BOM table, but formats, naming conventions, and component classifications were inconsistent across suppliers and drawings.

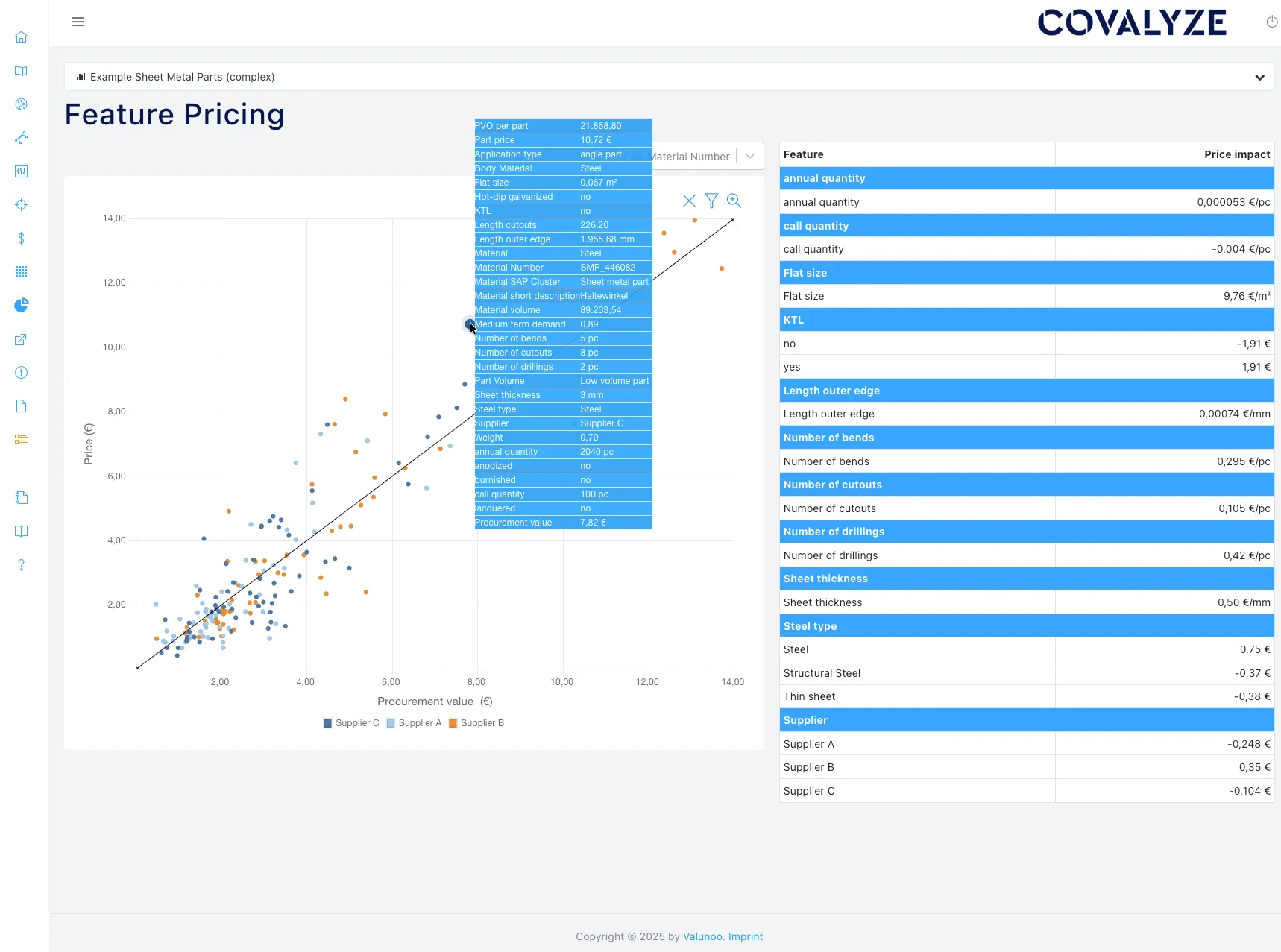

Using COVALYZE PartIQ and COVALYZE Analytics, the project team harmonized all BOM data, built component-level cost models, and created supplier-specific negotiation strategies grounded in commodity exposure and transparent benchmarking.

Key Figures

Bill-of-material tables extracted and harmonized across all suppliers.

Cross-supplier cost comparison enabled through standardized BOM structure.

Selected boards modeled at full component and process cost granularity.

Weighted commodity-driven cost increase across solder paste formulations.

Total spend covered by the structured analysis and negotiation model.

Bare board represented a consistent but secondary cost driver.

Problem Frame

The Challenge

When the procurement team received simultaneous price increase requests from multiple PCBA suppliers, each citing raw material cost pressures, the lack of standardized data made it impossible to assess whether the demands were justified.

Fragmented BOM Data

Although the project scope covered 45 PCBA variants, the underlying BOM tables were delivered in non-standardized formats across 3 suppliers. Each table used different conventions for:

- » Non-standardized column headers across BOM tables

- » Inconsistent component naming and classification

- » Mixed formats across 3 supplier quotations

- » No unified distinction between active and passive components

- » Missing or ambiguous solder paste and raw material references

- » No cross-part comparability between PCBA variants

Data Gap

Without harmonized BOM structures, the team could not compare component costs across suppliers or isolate the true impact of commodity price movements. Supplier claims of “raw material increases” remained unverifiable, leaving procurement in a reactive position.

The customer needed a systematic way to standardize disparate BOM data, model cost structures at the component level, and quantify which portion of each price increase was actually driven by commodities.

Execution Design

Our Approach

BOM Extraction & Harmonization

Using COVALYZE PartIQ, the project team extracted, standardized, and harmonized all 45 BOM tables into a unified cross-supplier data structure.

BOM Extraction

Through automated extraction of 45 BOM tables across 3 suppliers, the team captured all component references, quantities, and material specifications. Each board contained between 10–50 passive and 1–5 active components.

Data Harmonization

The team unified all BOM structures into a comparable format:

- » Unified column headers and component classifications

- » Standardized active vs. passive component tagging

- » Aligned quantity and unit-of-measure fields across suppliers

Cost Structure Mapping

For each variant, the team mapped the cost structure to four layers:

Technical Cost Modeling & Commodity Analysis

Using COVALYZE Analytics, the team built component-level cost models for 6–7 deep-dive designs and mapped commodity exposure across the full portfolio.

Component Cost Model

For each deep-dive design, the system determined:

- » Component-level price breakdown (active vs. passive)

- » Solder paste consumption and raw material content

- » PCB bare board cost allocation

Active components represented the largest single cost driver, while solder paste — though a smaller share — was the most volatile due to silver and tin exposure.

Commodity Exposure

Raw material costs were benchmarked against current commodity prices. Price dynamics over the previous 12 months:

Suppliers were requesting blanket price increases, but exposure varied significantly by component type and board design.

Commercial Implications

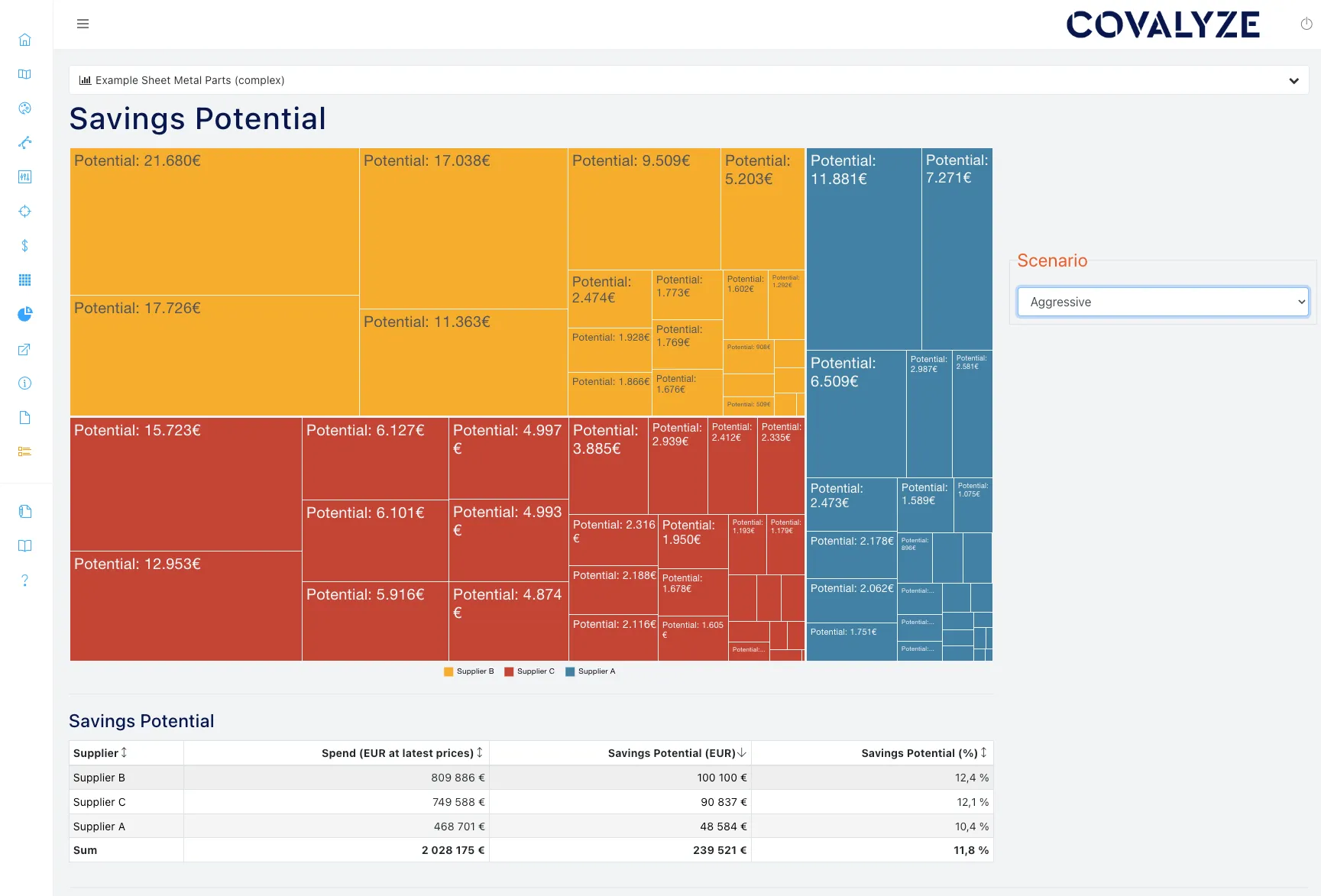

A full cost calculation across EUR 50 million in procurement volume, including supplier-level margin analysis, revealed:

Active components (ICs, microcontrollers) represented the dominant direct cost driver, with component prices accounting for the majority of total PCBA cost

Distributed across:

Supplier-Specific Negotiation Design

Based on the analysis, supplier-specific negotiation strategies were developed:

Isolating justified commodity pass-through from unjustified margin increases

Supplier-specific negotiation scripts based on individual cost exposure profiles

Cross-supplier benchmarking to identify pricing outliers and leverage competitive tension

Transparency Achieved

By harmonizing BOM data across all 45 PCBA variants and 3 suppliers, the team established a complete cross-part comparison baseline. For the first time, procurement could see exactly which cost elements were commodity-driven and which reflected supplier-specific pricing decisions.

Outcome & Impact

The Result

By harmonizing 45 BOM tables across 3 suppliers and building component-level cost models with full commodity traceability, the customer gained a fact-based foundation to challenge supplier price increases and steer negotiations proactively.

Negotiation Readiness

This enabled the organization to:

- » Separate legitimate raw material pass-through from discretionary price increases

- » Challenge supplier claims with component-level cost transparency

- » Compare cost structures across 3 suppliers on a harmonized basis

- » Prioritize negotiation actions by spend impact and commodity exposure

“What was previously a supplier-driven price discussion became a fact-based negotiation grounded in component logic, raw material exposure, and transparent benchmarking.”

Bill-of-material tables extracted and harmonized across all suppliers.

Cross-supplier cost comparison enabled through standardized BOM structure.

Selected boards modeled at full component and process cost granularity.

Weighted commodity-driven cost increase across solder paste formulations.

Total spend covered by the structured analysis and negotiation model.

Bare board represented a consistent but secondary cost driver.

What began as a reactive response to supplier price increases became a structured cost transparency and negotiation enablement program.

From Supplier-Driven Pricing to Fact-Based Negotiation

With harmonized BOM data, component-level cost models, and quantified commodity exposure, the customer moved from accepting supplier claims at face value to challenging them with structured evidence and supplier-specific negotiation strategies.